How to Lower RV Insurance Cost

Direct answer

How much does how to lower rv insurance cost cost?

How to Lower RV Insurance Cost is about understanding where coverage, exclusions, deductibles, limits and carrier rules can affect a household, property owner or business. The right answer usually depends on the property, assets, use case, claims history, risk tolerance and how the policy is written.

RV insurance premiums can vary widely depending on the type of recreational vehicle, its value, how often it is used, and the coverage options selected. Fortunately, there are several ways RV owners can reduce insurance costs while still maintaining strong protection.

Lowering RV insurance premiums usually involves a combination of coverage choices, deductible decisions, and eligibility for available discounts. Understanding how insurers calculate premiums can help owners structure their policies more efficiently.

If you are evaluating insurance options, it may also help to review how much RV insurance costs and available RV insurance discounts.

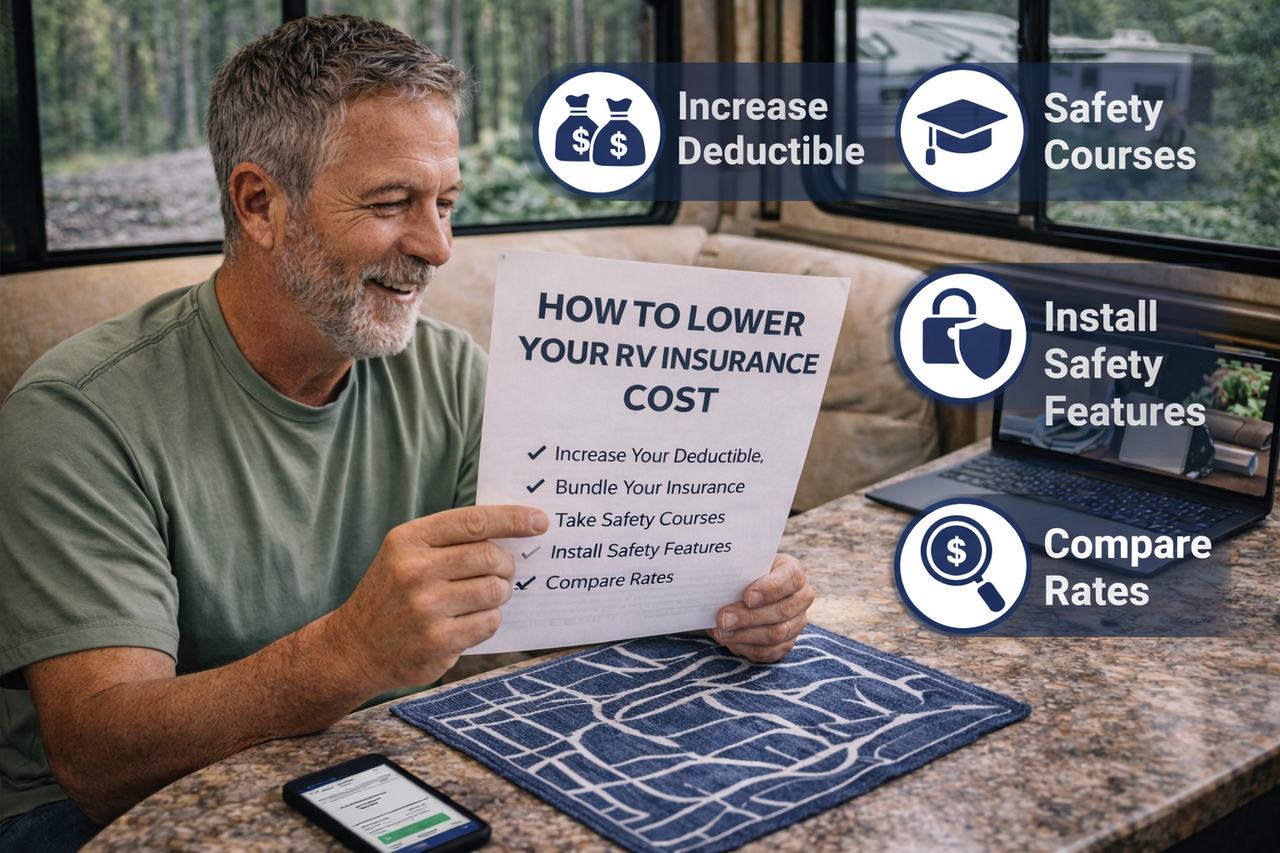

Increase your deductible

One of the most direct ways to lower an RV insurance premium is by increasing the deductible. The deductible is the amount the policyholder pays out of pocket before insurance coverage applies to a claim.

Choosing a higher deductible reduces the insurer’s potential payout on smaller claims, which often results in lower premiums.

- Higher deductibles usually reduce premiums

- Lower deductibles increase monthly or annual cost

- Deductibles should align with financial comfort level

To better understand how deductibles affect insurance pricing, review RV insurance deductibles explained.

Bundle policies with the same insurance provider

Many insurers offer multi policy discounts when RV insurance is bundled with other types of coverage such as homeowners insurance, auto insurance, or umbrella policies.

Bundling policies can sometimes reduce overall insurance costs across multiple policies.

- RV insurance combined with auto insurance

- RV insurance combined with homeowners insurance

- Multiple recreational vehicles insured together

For more details about available savings opportunities, see RV insurance discounts.

Choose the right coverage limits

Insurance policies often include several optional coverage components. Selecting coverage levels that match the actual value of the RV and personal risk tolerance can help control premium cost.

Common coverage components that affect price include:

- RV collision coverage

- RV comprehensive coverage

- Total loss replacement coverage

- Personal effects coverage

Reviewing these coverages carefully can help RV owners avoid paying for protection they may not need while still maintaining appropriate risk protection.

Use your RV seasonally

Many RV owners only use their vehicles during certain parts of the year. Some insurers offer lower premiums for recreational vehicles that are used occasionally or stored during the off season.

- Seasonal travel usage

- Limited annual mileage

- Secure storage during winter months

If your RV is primarily used for vacations or occasional travel, you may want to review RV insurance for seasonal use.

Improve RV security and storage

Insurance companies may offer lower premiums when the risk of theft or damage is reduced. RVs that are stored securely or equipped with safety features may qualify for lower insurance costs.

- Secure indoor storage facilities

- Anti theft devices

- GPS tracking systems

- Alarm systems or immobilizers

These risk reduction measures may make the RV less attractive to thieves and reduce potential claim exposure.

Maintain a clean driving record

Driver history plays a major role in insurance pricing. Drivers with fewer accidents and violations are generally considered lower risk by insurers.

- Avoid traffic violations

- Maintain safe driving habits

- Limit claims when possible

Safe driving history may also help qualify RV owners for additional premium discounts depending on the insurer.

Compare quotes from multiple insurers

Because insurance companies use different underwriting models and pricing strategies, premiums can vary significantly between carriers. Comparing quotes from several insurers can often reveal meaningful differences in pricing.

Working with an agency that can review policies across multiple carriers may help identify better coverage options and competitive premiums.

Location can influence RV insurance cost

Insurance premiums can also vary depending on where the RV is registered or stored. Regional factors such as weather exposure, theft rates, and claims frequency may affect pricing.

For location specific guidance, review:

Lowering RV insurance cost within the RV coverage structure

Lowering insurance premiums should always be balanced with maintaining appropriate coverage. Selecting the right coverage structure helps protect both the RV itself and the financial well being of the owner in the event of a claim.

Related RV insurance pages

Compare RV insurance options

Reducing RV insurance costs does not have to mean sacrificing important protection. Reviewing policy structure, exploring available discounts, and comparing quotes across multiple insurers can help RV owners identify policies that balance affordability and coverage.

Our agency helps RV owners evaluate insurance options and identify policies that align with their travel patterns, RV type, and financial goals.

Request your RV insurance quote

Coverage availability, limits, exclusions, deductibles, and eligibility vary by carrier and policy. This page provides general informational guidance and does not describe all terms or conditions of any specific insurance policy.

Frequently asked questions

What should I know about How to Lower RV Insurance Cost?

How to Lower RV Insurance Cost should be reviewed in the context of your actual risk, not only the lowest premium. Policy language, endorsements and carrier appetite can change the practical answer.

How can I avoid coverage gaps?

Share accurate property, vehicle, business or rental details with your agent, review exclusions and ask how deductibles and limits would apply in a realistic claim.

When should I request a review?

Request a review before renewals, after major purchases, after property changes, when adding rentals or vehicles, or any time your financial exposure changes.

Missouri and Kansas Insurance Agent

Work With Tracy Fitch

Missouri and Kansas clients can work with Tracy Fitch, a property and casualty licensed insurance agent with more than a decade of insurance experience. Tracy helps clients review coverage, compare options, request policy changes, and understand next steps for home, auto, landlord, umbrella, renters, boat, RV, and business insurance.

Office: 212 W Mill St, Liberty, MO 64068

Email tfitch@hensonagency.com or call 816-479-4189.