Homeowners Insurance Deductible Guide

Choosing the right homeowners insurance deductible is one of the most important decisions in your policy. Your deductible directly affects your pre

Quick Answer A homeowners insurance deductible is the amount the policyholder pays on a covered claim before insurance pays. Deductibles can be flat dollar amounts or percentage-based, and wind or hail deductibles may work differently. A homeowners insurance deductible is the amount the policyholder pays on a covered claim before insurance pays. Deductibles can be flat dollar amounts or percentage-based, and wind or hail deductibles may work differently. A good insurance review should compare the real exposure, not just the lowest premium. For Missouri and Kansas clients, that usually means reviewing policy limits, deductibles, exclusions, carrier appetite, proof-of-insurance requirements and how the coverage fits with other policies. Henson Agency helps clients compare coverage details across available options so the decision is easier to understand. The goal is to avoid underinsuring the risk, overpaying for coverage that does not fit, or missing a requirement from a lender, landlord, marina, lease, contract or property manager. One common mistake is assuming every policy form handles the exposure the same way. Deductibles, exclusions, coverage triggers, named insureds, additional interests, loss payees and liability limits can change the value of the policy. Another mistake is waiting until a closing, lease signing, marina renewal or lender deadline to review insurance. Starting early gives the agency more room to compare carrier options and fix documentation issues. Review coverage before a purchase, renewal, lease, lender request, claim concern or major change in how the property or vehicle is used. Yes. Henson Agency can help Missouri and Kansas clients compare available coverage options and understand next steps. Not always. Price matters, but the coverage form, limits, exclusions, deductible and proof requirements matter too.Homeowners Insurance Deductibles: What to Know First

How to Compare This Coverage

Decision Checklist

Common Mistakes to Avoid

Related Coverage Guides

Homeowners Insurance Deductibles FAQs

When should I review homeowners insurance deductibles?

Can Henson Agency compare options?

Is the cheapest policy always best?

This guide explains how homeowners insurance deductibles work, how to choose the right amount, and how deductibles interact with premiums, claims, and long term insurance costs.

Request a Home Insurance Review

What Is a Homeowners Insurance Deductible?

A homeowners insurance deductible is the amount you agree to pay out of pocket before your insurance policy pays for a covered loss. The deductible applies to most property claims and is subtracted from the claim payout.

For a full understanding of how policies are structured, you may want to review the homeowners insurance overview.

For example, if you have a $2,500 deductible and a covered loss of $15,000, you would pay the first $2,500 and the insurance company would pay the remaining $12,500.

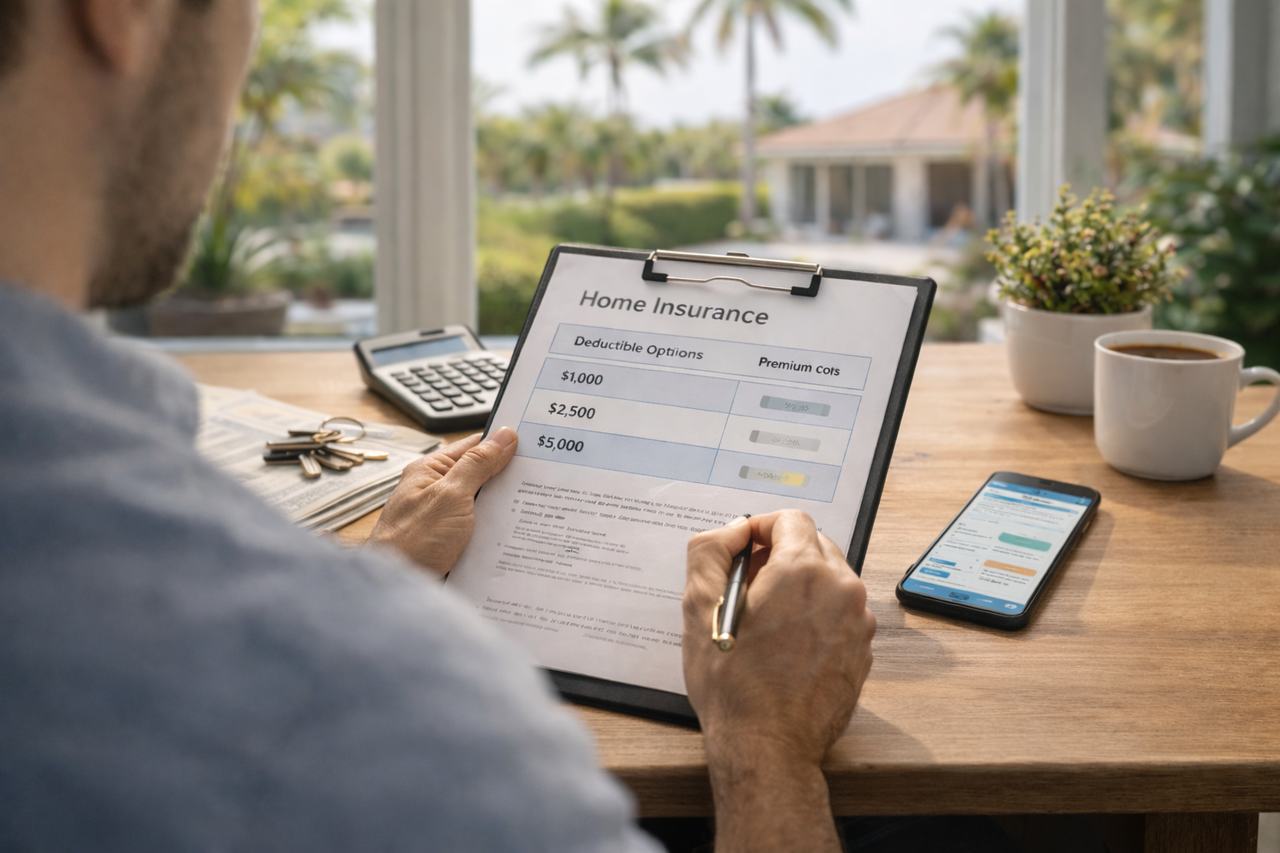

Common Home Insurance Deductible Types

Flat Dollar Deductibles

This is the most common deductible type. Examples include $1,000, $2,500, or $5,000. Flat deductibles are predictable and easier to budget for.

Percentage Deductibles

Some policies use percentage based deductibles, especially for wind or storm related claims. These are calculated as a percentage of your home’s insured value.

Understanding how these apply is especially important in storm-prone areas. See windstorm and hurricane coverage.

For example, a 2 percent deductible on a $400,000 home equals an $8,000 deductible.

Separate Wind or Hail Deductibles

Certain policies apply a different deductible for wind, hail, or named storm losses. These deductibles can significantly affect your out of pocket costs during major claims.

How Deductibles Affect Your Premium

In general, higher deductibles lower your insurance premium, while lower deductibles increase premium cost.

- Lower deductible: Higher premium, lower out of pocket cost during a claim

- Higher deductible: Lower premium, higher out of pocket cost during a claim

This tradeoff is a key part of your overall cost strategy. For additional pricing context, see how much homeowners insurance costs.

How to Choose the Right Deductible

When selecting a deductible, consider the following:

- Emergency savings available

- Likelihood of filing smaller claims

- Age and condition of the home

- Roof age and storm exposure

- Premium savings compared to deductible increase

Homes with higher risk factors may require a different approach. If your property has aging systems, review insurance for older homes.

Deductibles and Claim Strategy

Insurance works best for larger, unexpected losses. Filing frequent small claims near the deductible amount can increase future premiums or limit carrier options.

A properly chosen deductible helps preserve your policy for major events such as fires, severe storms, or significant liability situations.

To understand how claims are evaluated and paid, review the homeowners insurance claims process.

How Deductibles Relate to Coverage Gaps

Deductibles only apply to covered losses. If a loss is excluded, the deductible does not apply at all.

For example, flood damage is typically not covered under standard homeowners policies. Learn more about flood vs homeowners insurance.

Understanding both deductibles and exclusions is critical to avoiding unexpected out of pocket costs.

Deductibles vs Discounts and Savings Strategy

Increasing your deductible is one way to reduce your premium, but it is not the only approach.

You may also benefit from structured pricing reductions such as homeowners insurance discounts.

For broader cost strategies beyond deductibles, see ways to save on homeowners insurance.

Missouri and Kansas Deductible Considerations

Homeowners in Missouri and Kansas often balance deductibles with exposure to wind, hail, and seasonal weather events.

Understanding how storm deductibles apply before a loss occurs is critical in these regions.

For local guidance, explore:

How Deductibles Fit Into Your Overall Protection Strategy

Your deductible is just one part of your overall protection structure. It works alongside coverage limits and liability protection.

If you are evaluating higher liability exposure, you may also want to review how umbrella insurance extends homeowners coverage.

Related Homeowners Insurance Guides

Request a Home Insurance Review

If you are unsure whether your deductible is appropriate, we can review your homeowners policy, explain your options clearly, and help you balance premium savings with financial protection.

Request Your Home Insurance Review

Coverage availability, deductibles, and underwriting guidelines vary by carrier and policy. This page is for general informational purposes only.

Frequently asked questions

What should I know about Homeowners Insurance Deductible Guide?

Homeowners Insurance Deductible Guide should be reviewed in the context of your actual risk, not only the lowest premium. Policy language, endorsements and carrier appetite can change the practical answer.

How can I avoid coverage gaps?

Share accurate property, vehicle, business or rental details with your agent, review exclusions and ask how deductibles and limits would apply in a realistic claim.

When should I request a review?

Request a review before renewals, after major purchases, after property changes, when adding rentals or vehicles, or any time your financial exposure changes.

Missouri and Kansas Insurance Agent

Work With Tracy Fitch

Missouri and Kansas clients can work with Tracy Fitch, a property and casualty licensed insurance agent with more than a decade of insurance experience. Tracy helps clients review coverage, compare options, request policy changes, and understand next steps for home, auto, landlord, umbrella, renters, boat, RV, and business insurance.

Office: 212 W Mill St, Liberty, MO 64068

Email tfitch@hensonagency.com or call 816-479-4189.